Leonard Shatzkin (1920-2002) was a distinguished figure in the world of book publishing and bookselling.

Initially trained in printing, he joined Doubleday and eventually became its Director of Research, pioneering the use of quantitative methods in book production, inventory and sales forecasting.

In his monograph, The Mathematics of Bookselling, Shatzkin draws together his decades of experience to create a clear and rigorous framework that demonstrates how booksellers can improve profitability. He notes the ways this can be done through better buying decisions, sharper inventory management and faster turnover of stock.

For any book retailer serious about improving margins and optimising investment in stock, his ideas remain both timely and actionable, despite the book being written in 1997.

All references and quotes within this article come from ‘The Mathematics of Bookselling’, by Leonard Shatzkin, 1997.

What is stock turn?

Stock turn is a term that appears again and again in Shatzkin’s book. It’s a key metric that describes how many times a bookseller sells through and reinvests each dollar (or pound) of inventory over a given period (usually one year).

In Shatzkin’s terms, stock turn is a measure of how long books sit in the store before being sold and how efficiently the working capital is being used. It can only be calculated at the end of the sales period, but the outcome can be used to determine your future bookselling strategies.

So how do you work it out?

First, you need the total cost of goods sold (COGS) during one year.

Then, you need to find the average inventory value. Add your opening inventory value to your closing inventory value and divide this by two.

Finally, divide the first number by the second number, and this will show how many times you sold and replaced your entire inventory during that year. Shatzkin emphasises that a higher stock turn means each invested dollar in inventory is being freed up sooner, enabling reinvestment into new titles or other operational needs.

The importance of stock turn is that it sits alongside margin to determine return on investment. Buying a title at a good margin is useful, but if the stock remains unsold for months, the return is eroded by time, cost of capital and the opportunity cost of not investing those funds elsewhere.

As Shatzkin puts it, “The longer you keep books in the store, the less they contribute to the rate of profit when they are sold” (p. 26).

In short, stock turn = speed × efficiency of inventory investment. Understanding and improving this metric enables booksellers to harness their working capital more effectively and drive higher profits.

While Shatzkin covers a lot of ground in his 59-page monograph, we’ve summarised his points into six key takeaways that capture the heart of his thinking.

1. The core metric: margin x turn

Shatzkin emphasises that the economic health of a bookstore hinges “more on what titles are bought and, even more important, how they are bought than on anything else the book retailer does” (p. 5).

In the opening pages, he defines a crucial metric: the gross margin return on inventory investment (GMROII), which is computed as margin (how much you make per book) multiplied by stock turn.

“Stock turn is the measure of how long books sit in the store before they are sold [...] It is a measure of the productivity of working capital. It is a measure of how much sales a dollar of inventory will produce in any unit of time” (p. 9).

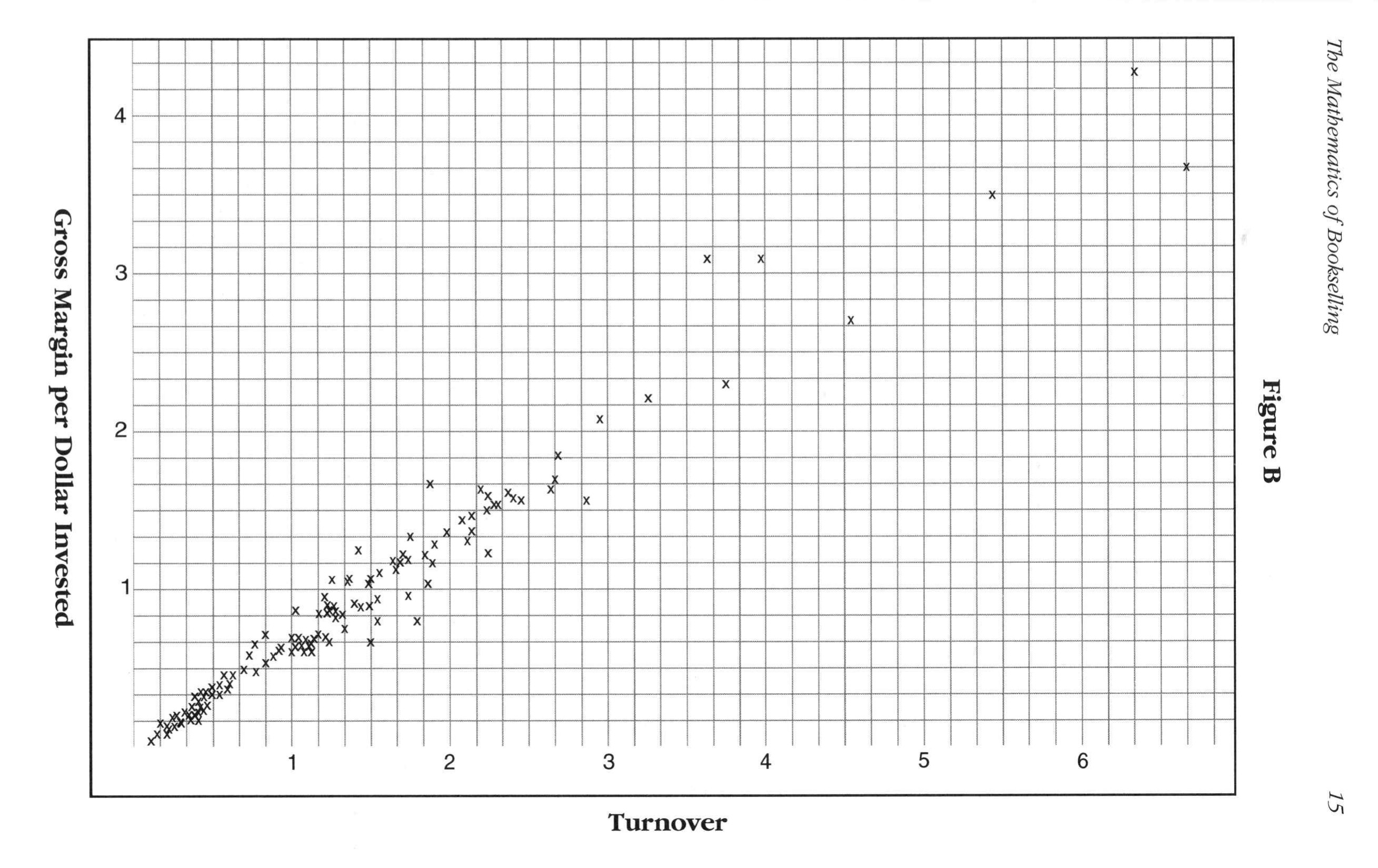

To put it plainly, purchasing a book at one price and selling at another gives you margin, but if that money sits on the shelf for months (money is tied up in the book that won’t sell), the opportunity cost is high. A high margin on slow-moving stock doesn’t necessarily beat a modest margin on fast-moving stock. Shatzkin’s graph (p. 15) shows clearly that the lower the stock turn, the lower the GMROII.

Application for booksellers today:

Don’t just track discount or margin, but how fast inventory is coming back as cash. If a title takes six months to sell, the cost of tying up that capital may outweigh the margin benefit of heavy discount.

Prioritise the titles you know will turn quickly. These may be consistent sellers, predictable demand and categories you understand.

Use the metric “money invested in stock → money realised per year” as your benchmark, rather than simply focusing on discount.

2. Discount is not the be all and end all

One of Shatzkin’s most engaging (and possibly controversial) insights is how discounting works with (or against) stock turn. He notes that publishers offer larger discounts to encourage larger orders from the bookseller, but that this incentive only pays off if the increased discount doesn’t slow down stock turn proportionally.

He writes:

“If, on a larger order, the increase in discount results in an increase in margin of 10% and it takes less than 10% longer to sell the books in the larger order, the bookseller will be richer; [...] if it takes more than 10% longer to sell the books, the bookseller would be better off with the original order” (p. 10).

This principle can be applied practically when looking at two university presses, Harvard and Yale.

In 1982, they both had similar inventory investment. Harvard averaged a discount of 38.6%, compared to Yale’s 43.7%. To a bookseller, it seems most logical to purchase from Yale at a higher discount. However, Shatzkin points out that the return per dollar invested in inventory was almost twice as great from Harvard titles as from Yale titles. This is because the stock turn for Harvard was double that of Yale. The books shifted faster so, despite paying more for them, the return on investment was captured more quickly (p. 16).

So what’s the takeaway? Discounting may look attractive initially, but if it slows the turnover of investment, then the net result may be worse.

What to watch for:

Be wary of large orders driven purely by discount thresholds (e.g. you get 40% off if you purchase 100 copies) unless you are very confident you can shift them. Instead, consider making smaller orders more frequently. The discount won’t be as much, but this isn’t necessarily an issue if those books sell in days rather than months.

Use turnover to track margin. If your bulk order drags out for months, you’ll lose margin in the long run.

Aim for minimal commitment when it comes to less familiar categories or slower movers.

3. Buying frequency, quantity and working capital

Perhaps the most practical and actionable theme in Shatzkin’s work is the recommendation to buy more frequently in smaller quantities than infrequently in large amounts.

He says:

“The longer you keep books in the store, the less they contribute to the rate of profit when they are sold. [...] The objective is to minimize the time between receipt and sale of any book. The easiest and least expensive way to sell books closer to the day they come in is to buy books closer to the day they are sold” (p. 26).

It’s clear that that’s every bookseller’s dream — to sell as soon as it lands. This clearly can’t always be the case, but Shatzkin notes that the easiest way to do this is to purchase books every day:

“Although most booksellers buy every day, they buy for a longer term, tying up more money on each title than they need to tie up [...] Buying the more active titles every day to meet immediate needs [...] can do wonders for your stock turn, your working capital, and your cash flow. Buying every day can get you stock turns of 30 or 40 times on bestsellers with ease…” (p. 35).

If you order lots of stock and let it sit, you’re using up your working capital inefficiently. If, instead, you order just enough for near-term demand and restock frequently, you free up capital, reduce risk of obsolescence or slow sales, and improve turn.

In today’s bookselling climate — with online ordering, drop-ship options, sophisticated inventory systems — this principle is even more applicable.

So how can you implement this in real-life bookshops?

Analyse your bestselling titles using your PoS and stock management software. What is the time-to-sale? How often could you reorder in small quantities rather than over stock?

Use replenishment frameworks (e.g. make an initial small order followed by a rapid reorder once you see real demand). Shatzkin talks about immediate response vs. delayed response titles:

Immediate response titles are those with highly anticipated demand. You might order a few initially and then replenish.

Delayed response titles are those you expect to sit on a shelf or sell slowly. Buy one copy and then monitor for reorder.

Use wholesalers (or rapid-turn suppliers) for quick reordering. Shatzkin argues that smaller, more frequent orders cost more in clerical overhead but those costs are minor compared to the cost of slower stock turn (p. 30).

Align your buying rhythm with your actual sales rhythm. Don’t buy for the next six weeks when only two weeks’ worth of demand is predictable.

4. Breadth of inventory and category discrimination

Another dimension Shatzkin explores is the trade off between breadth of titles in stock and depth or quantity of each title. He cautions that under-ordering titles purely to improve turn may harm the store’s appeal. For instance:

“If the overall stock turn is four, but the turn in the biography category is two and mysteries is eight, biography is distinctly less a candidate for adding titles than is mysteries [...] Categories that have a lower stock turn, like (in this case) biography, are by no means necessarily candidates for reducing the number of titles [...] Broad inventory [...] acts to make the store more attractive and to help sell books in all categories” (p. 34).

This can be a little contradictory. Keeping the categories that aren’t moving that quickly may slightly reduce stock turn, and yet they’re still necessary.

But what you can do is use this to control the types and quantity of books you’re publishing. Invest more in those fast-turning categories that you know will sell, but be a bit more cautious with those slow-turning categories. They still have value (store identity, diversity, customer attraction) but should perhaps be purchased in lower quantities.

Shatzkin has a good solution to the problem whereby the weakest titles (those with low stock turn) should be identified and flagged as “do not reorder” (p. 33).

For today’s booksellers:

Use your data to calculate category-by-category and title-by-title turns (sales divided by average inventory)

Identify titles with persistently low turn and ask whether they are critical to your store image or simply dead weight (if the latter, don’t reorder)

Maintain a selective range of slower-moving titles if they contribute to the uniqueness of your shop or customer loyalty. You should recognise that the goal is total profits, and not just average margin or turn.

Balance is key and a narrow, high-turn category may yield high return but limits appeal. Whereas a broad catalogue with some slower titles can enhance footfall and cross-selling opportunities (they purchase more than they came in for).

5. Returns, risk and purchasing responsibility

Shatzkin offers an unflinching view of the risk of returns and the cost to booksellers. He makes excellent points on returns, the most notable being:

“The right to return was created by the publisher and for the publishers”

“Returns cost the bookseller much more than they cost the publisher” (p. 51).

It’s a system that was designed during the depression of the 1930s to encourage booksellers to continue investing in their inventory, safe in the knowledge that they could get some of that investment back when they returned unsold stock. It was a win-win for both booksellers and publishers.

However, he does note that you should proceed with caution. The system can very easily become corrupt when booksellers purchase huge quantities of books they know they can’t shift. While the return policy does protect you, over-ordering is risky. It ties up capital, invites obsolescence and shifts the risk onto the retailer (you).

Shatzkin contends that smart buying methods can reduce return rates (which should always be a goal) and extend the breadth of title assortment.

For bookshops:

Treat your ‘right to return’ as a safety net and not a justification for large, speculative orders

Monitor your return rates by title and use that as an indicator for future purchases

Use data (your own sales pattern or historical turn) to inform orders rather than going off sales rep enthusiasm or publisher push.

6. The case for data, prediction and automation

Finally, Shatzkin anticipates a future (and present) in which bookselling is informed by data rather than purely by gut or supplier persuasion.

He talks passionately about a mathematical predictor, a computer that could predict in advance the sales of every title in your bookshop. The issue here lies in the data collection required to make such a predictor, and data across hundreds or even thousands of bookshops would be necessary.

He writes:

“The substantial value of such information — depending on the number of independents [bookshops] involved, the advantages could run to millions of dollars annually — suggests that someone [...] will come forward to organise the gathering of sales information to make mathematical prediction routine” (p. 41).

A programme like this could continuously adjust its rules, reorder when titles sell, account for seasonal bias and relieve management of much of the routine decision making. He notes that:

“The goal of true computer ordering should be [...] to achieve the highest possible stock turn with a minimum incidence of being out of stock on better selling titles, and with a minimum commitment of management time” (p. 43).

In the current era of online retail, multi-channel fulfilment, automated inventory systems and rich analytics, these concepts are highly actionable. Even small independent bookstores can leverage sales data, supplier dashboards, and order-trigger systems.

Conclusion

Leonard Shatzkin’s The Mathematics of Bookselling offers a crisp, rationale-based solution for booksellers who wish to move beyond intuition, discount wars and bulk ordering into a more disciplined, data-informed, high-return model.

The key takeaways are:

Focus on margin x turn rather than margin or discount alone

High discounts or large bulk buys aren’t automatically better, particularly if they compromise turnover

Buy small, buy often, particularly for predictable sellers

Use data to identify slow-turn titles, but recognise that these still have their value (breadth of titles, store identity, etc)

Treat your returns strategically instead of using them as a safety net

Use data, forecasting and reorder automation to sharpen buying decisions.

For booksellers today, the digital age offers tools that Shatzkin could only anticipate: sophisticated inventory management, real-time sales data, predictive analytics and online replenishment.

The fundamental logic remains the same: working capital invested in books must earn a return, and one of the strongest levers to accelerate that return is faster stock turn. As you plan your buying and stock strategy, ask: “How many times will this pound I invest come back this year?”

That question — central to Shatzkin’s argument — might just be the difference between a store that survives and one that thrives.